Economics

Monthly UK Economic Outlook: September

Our economists share their views on the key economic trends to watch in the month ahead.

07 Sep 2023

. 4 min read

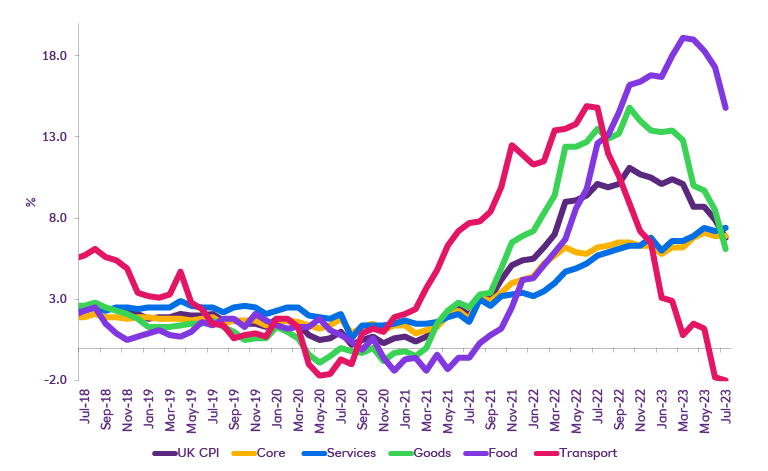

With slowing inflation, the Bank of England may be near the end of its rate-hiking cycle – welcome news for consumers and businesses alike. But from an economic perspective, is the damage already done?