Economics

Could electric vehicles be adding to trade tensions?

With signs of hidden protectionism under the veil of going green, what’s going on in the EV market?

26 Oct 2023

. 4 min read

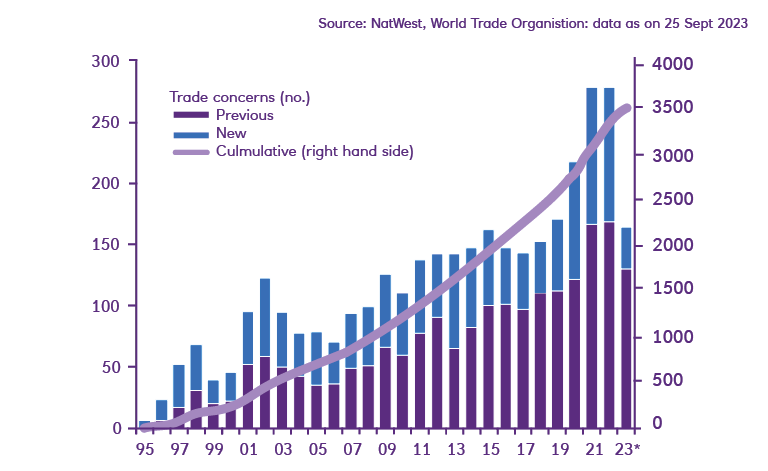

Trade protectionism is on the rise. Geopolitical tensions have started to weigh on trade, and are causing a fragmentation of global supply chains into localised ecosystems.