Finances

Tough Supply Chain Decisions for Future Fitness

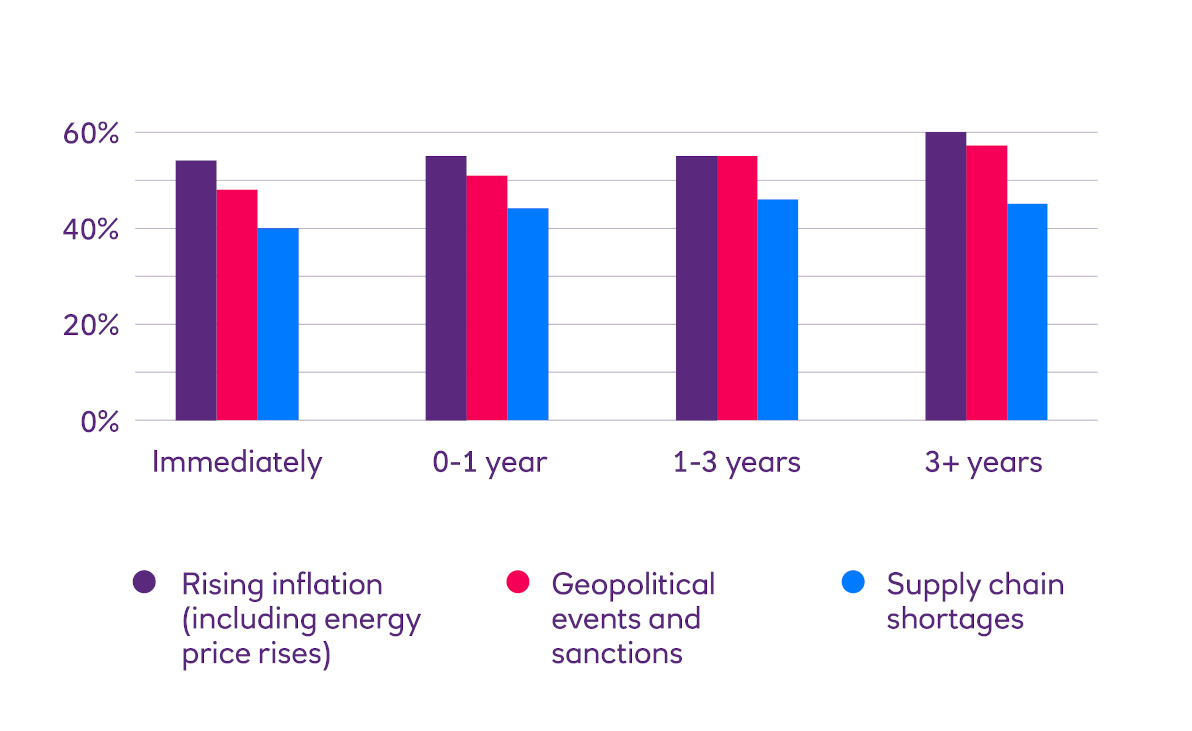

Finding a balance on competing objectives is essential as inflation and geopolitics continue to disrupt global supply chains.

10 Feb 2023

. 3 min read

Business decision-makers know there is rarely a perfect solution that meets today’s needs while setting you up for the future. When it comes to supply chains, though, it can be particularly tough.