Sector trends

The future of UK food and drink trade

As the UK seeks to become a greater trading nation, what are the export opportunities for the country’s food and drink industry? Jess Corsair, Trade and Policy Analyst from the Agriculture and Horticulture Development Board (AHDB), explains.

01 Jun 2022

. 4 min read

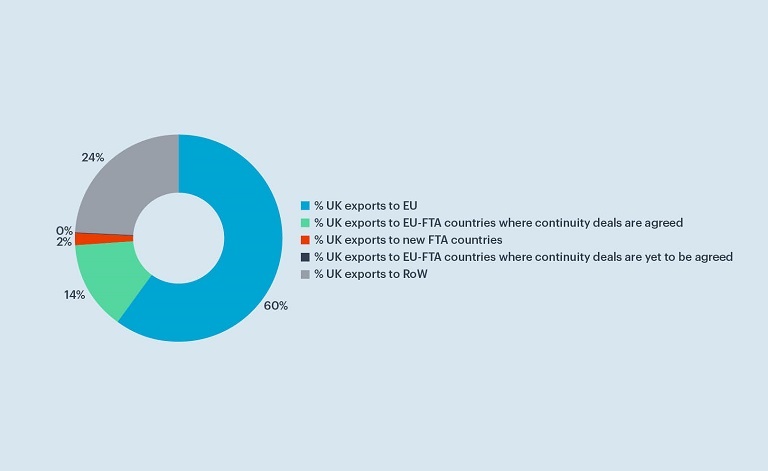

Post-Brexit, the UK is forging ahead arranging new trade deals likely to focus on items such as processed food and high-value cuts of meat. Meanwhile, the expanding global population may give rise to more affluent customers looking for goods that appeal to a larger middle-income group.

Picture credit: © Getty Images