The biggest difficulty for many mobility and logistics businesses is their supply chains. While the disruption seen at the height of the Covid-19 pandemic may have eased, 48% of the companies surveyed see shortages and disruption as likely to cause them significant issues in the medium term.

For many, the difficulties are already here. They’re struggling to secure the materials and parts they need – the chip shortage in the automotive sector has been a headache globally, for example – and prices are rising rapidly as inflation spirals, causing cashflow problems.

“Our biggest learning is that you have to talk about it rather than waiting until it becomes a problem,” says Matthew Grainger, CEO at Grainger & Worrall Technologies, a Midlands firm that makes automotive components for high-performance vehicles. “If you are open and transparent with stakeholders, including your customers, it is in everybody’s interest to find solutions.”

For example, customers may be willing to settle bills more quickly if a key supplier is unlikely to be able to cope with pricing pressure in its supply chain. In some cases, larger businesses are even helping smaller firms to invest in new in-house capacity or to reorient their supply chains.

The other constituency to focus on, says Alison France, Director at Green 4 Motor Company in Coventry, is the customer base. Her business serves consumers – selling them cars or repairing their vehicles – and has had to work hard to make sure they understand exactly when and why there might be delays.

“Customers haven’t got annoyed because we’ve kept them informed,” Alison says. “We’ve just been as honest and open as we possibly can.”

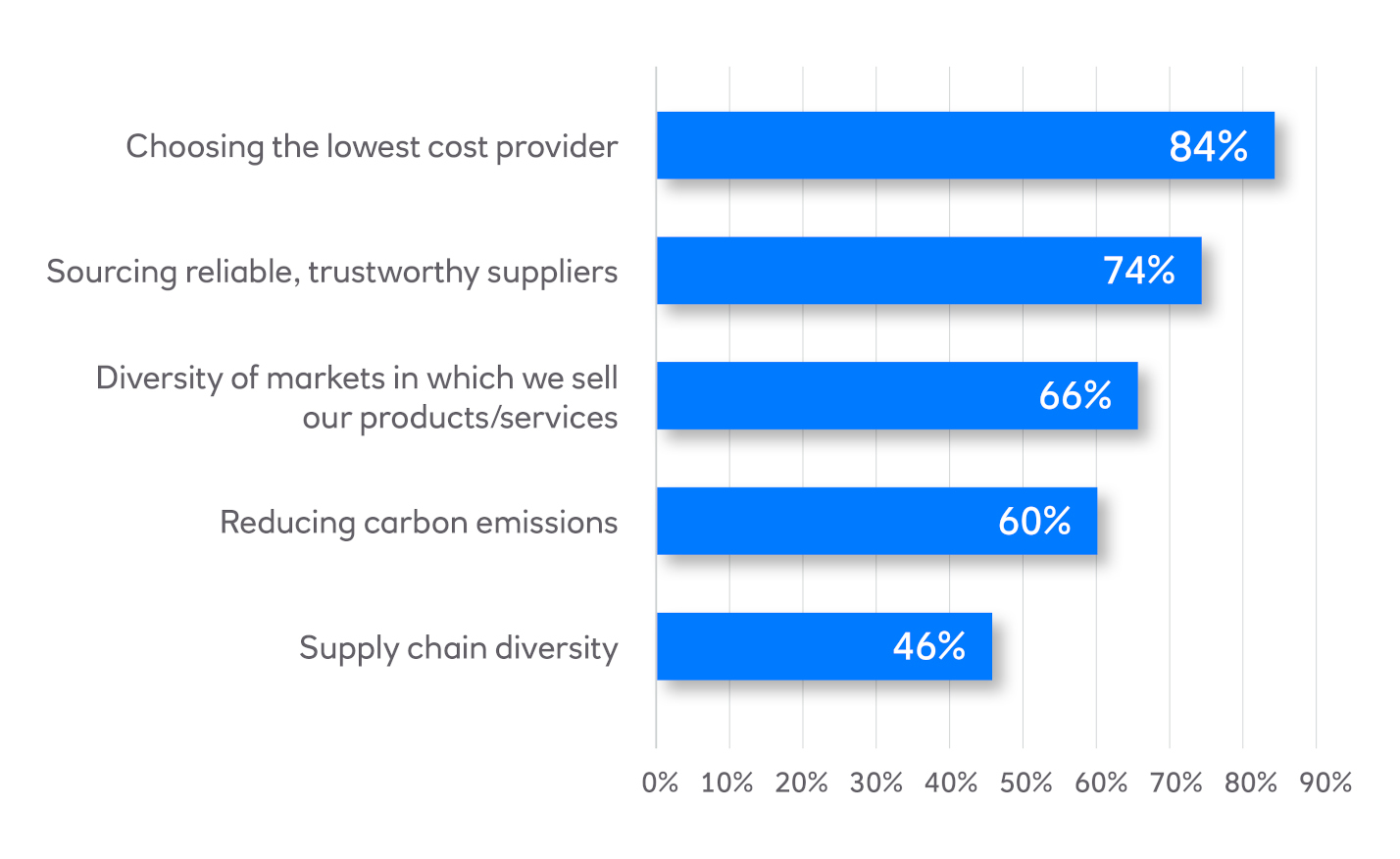

Matthew believes the supply chain crisis is an opportunity to rethink relationships throughout the industry. In our research, 84% of mobility and logistics businesses say low cost is their key demand of suppliers. By contrast, only 46% are concerned about supply chain diversity and only 54% agree that supply chain diversity supports resilience (see chart below).

How important are the following when considering suppliers? (% of mobility and logistics respondents)